16.5% of Businesses Experienced Little or No Effect from Pandemic, 55.3% Expect Long-Term Challenges

The U.S. Census Bureau’s Small Business Pulse Survey (SBPS) started asking businesses in April of last year when they expect to return to normal levels of operations, a crucial indication of how they are adapting to the pandemic, social distancing, and other public health strategies.

The SBPS, which has provided near real-time information on how small-single-location-employer businesses have been faring since late April when it began collecting data, has now concluded its third phase.

Business expectations about the future of the economy, customer demand, and the availability of supplies and inputs impact key decisions from hiring to investing.

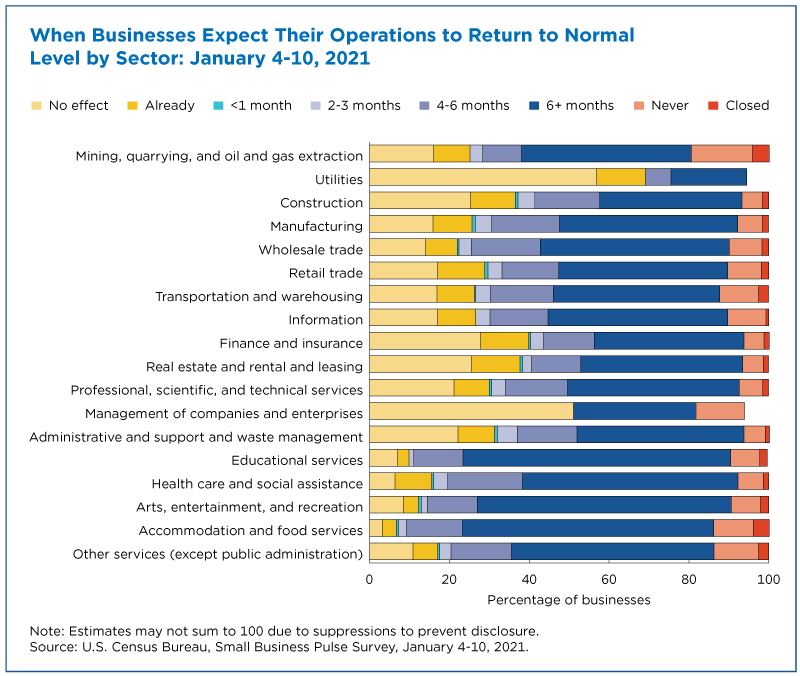

Sectors with relatively high percentages of businesses not affected by the pandemic or that already returned to normal level of operations include construction, finance and insurance, real estate, and administrative support.

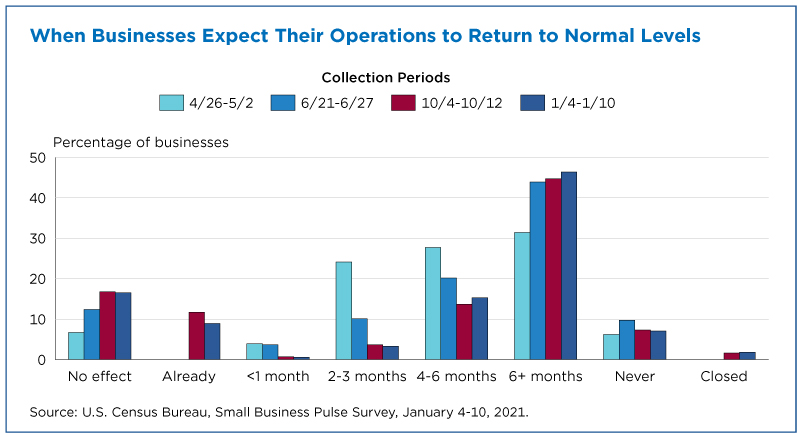

From spring to winter, business expectations of a return to normal level of operations have shifted so that there are many businesses with expectations at opposite extremes: businesses with expectation of a short-term return to normal and those facing long-term challenges.

Expectations moved away from the medium-term horizon of two to six months to either the short-term horizon (little or no effect, already back to normal, or less than one month to normal) or the long-term horizon (more than 6 months, never, or business has closed) (Figure 1).

Care must be taken when interpreting changes over time as other factors, such as business survival and surveying only those businesses with email addresses, can bias the responses and two categories (“already” and “closed”) were added in the later weeks of the survey, potentially altering the distribution of responses across other categories.

Expectations Differ by Sectors

Equally interesting are the differences in expectations across economic sectors.

Sectors with relatively high percentages of businesses not affected by the pandemic or that already returned to normal level of operations include construction, finance and insurance, real estate, and administrative support (Figure 2).

Here we have stacked responses from no effect/already returned to normal (shades of yellow), through longer durations of time (shades of blue), ending with never/business has closed (shades of red).

At the other end of the spectrum of expectations, sectors affected by the pandemic reporting the most concern about returning to normal levels of operations include educational services; arts, entertainment, recreation; and accommodation and food services.

Why Expectations Differ from Sector to Sector

Relative optimism in construction and real estate may reflect the fact that housing starts, construction, and completions have stayed relatively strong over the past few months. Private sources of data highlight the strong demand for housing likely partly in response to increased teleworking and remote education amid the pandemic.

Likewise, finance and insurance businesses may have more optimistic expectations because they rely heavily on digital and online transactions, which has allowed them to continue to operate as usual.

Other sectors, such as educational service businesses, were more likely to face challenges given their reliance on face-to-face interactions.

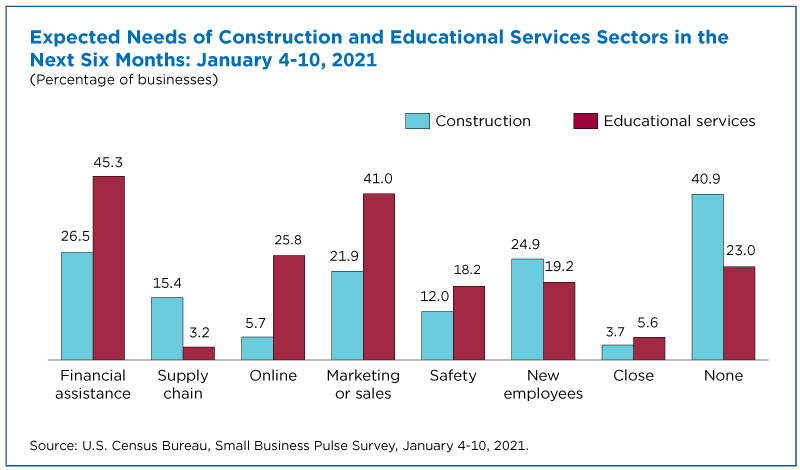

Focusing on two sectors with expectations at opposite ends of the spectrum, construction and educational services, provides insights into operating capacity and constraints:

- 72.1% of businesses in educational services experienced a decline in capacity with “physical distancing of customers or clients” the most cited reason for capacity constraints (36.1%).

- 44.5% of businesses in construction experienced a decline in operating capacity but only 11.0% indicated “physical distancing of customers or clients” impacted operating capacity.

In response to our question about future needs over the next six months, 5.6% of the businesses in educational services and 3.7% in construction expected they will “permanently close” (see Figure 3).

A higher fraction of businesses in educational services than in construction expect to need to obtain financial assistance, increase online presence, increase marketing or sales, and better provide for customer and employee safety.

Additional Surveys on Business Information Available

Data are available for downloads and for readers interested in business expectations, the Census Bureau collected information on business expectations as part of another survey, the Management and Organizational Practices Survey (MOPS), with results recently published in a working paper.

For a historical view, the Plant and Equipment Survey collected business expectations for about 40 years before ending in the 1990s.

Related Statistics

-

Stats for StoriesSmall Business Saturday: November 29, 2025In 2023, there were 8,361,342 U.S. business establishments. Most (7,152,312) had 19 or fewer employees, according to the CBP.

-

Stats for StoriesSmall Business Week: April 30-May 6, 2023The 2020 County Business Patterns found that 4.4M of all 8.0M establishments in the U.S. had 1 to 4 employees. Just under 200,000 had 100 employees or more.

Subscribe

Our email newsletter is sent out on the day we publish a story. Get an alert directly in your inbox to read, share and blog about our newest stories.

Contact our Public Information Office for media inquiries or interviews.

Related America Counts Stories

-

America Counts StoryFood Trucks: One Way to Eat Out During PandemicSeptember 02, 2020The food truck industry by its very nature is able to operate despite social distancing rules and no-indoor seating orders for restaurants during COVID-19.

-

America Counts StoryNew Small Business Pulse Survey Shows COVID-19 Impact on BusinessesMay 14, 2020The U.S. Census Bureau’s Small Business Pulse Survey yields near real-time economic data on businesses...

-

America Counts StorySelf-Employed Hit Harder by Pandemic Business Dip in Hard-Hit StatesJune 30, 2020Combining the experimental Household and Small Business Pulse surveys reveals demographic differences in the impact of pandemic on self-employed workers.

-

Families and Living ArrangementsOver a Third of Partners in Opposite-Sex Couples Were the Same AgeApril 27, 2026A new interactive data visualization explores characteristics of opposite-sex married and unmarried couples who lived together in 2025.

-

PopulationEight of the Nation’s Top 15 Last Names Stayed the Same Since 1790April 14, 2026Newly released names data from the 2020 Census show which first and last names are the most popular across the nation.

-

AgeU.S. Population Aging as Nation Turns 250April 09, 2026New population estimates show women still outnumbered men at older ages, but the gap is narrowing due to lower mortality rates and historical factors.

-

Business and EconomyState Lottery Ticket Sales Soar as Prizes Get LargerApril 08, 2026While sales nearly doubled to $104.7 billion from 2008 to 2024, state lottery prizes more than doubled to $70.2 billion in FY 2024.